How emergency funds deliver peace of mind

When life tosses up an unexpected event – such as retrenchment, a medical emergency or even just a big bill […]

When life tosses up an unexpected event – such as retrenchment, a medical emergency or even just a big bill […]

Debt is a common financial obligation that many people face. It refers to money borrowed from a lender that must

Over the past month, we have seen the Reserve Bank of Australia (RBA) pause its seemingly endless increase in cash

Whether considering options for yourself or deciding how best to help someone close to you, residential aged care can be

Ok so the heading sounds great, and who wouldn’t want more cash? With rising interest rates and general market uncertainty,

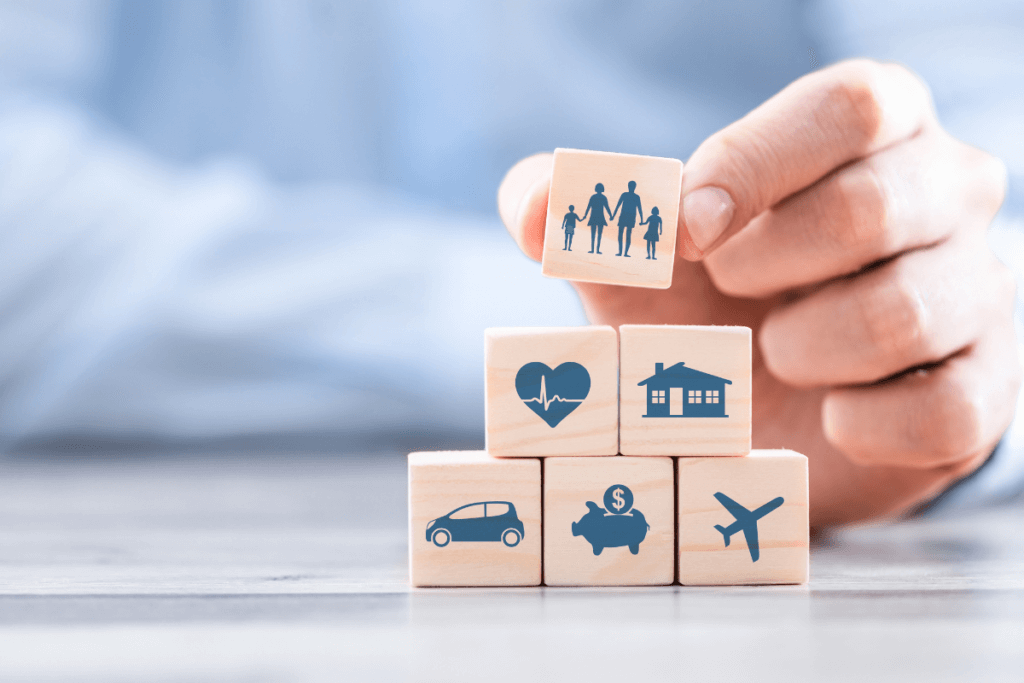

Many Australians hold some form of personal insurance, with many of us choosing to hold insurance through our superannuation provider.

We plan for many aspects of our lives, but few people plan for future aged care needs. Now is the

If you said, “they are all difficult to predict,” you would be right. Although, of all three, Molly is the

It is almost Christmas, so it is time for the present wishes; Lower inflation Lower interest rates Share market bounce

Have you heard the news? Inflation is skyrocketing in Australia and across the globe. Why? Governments have been printing and