The Australian Government has announced that the pension halving legislation originally announced on 1 July 2019 will continue for a further 12 months. It is now scheduled to finish on 30 June 2023. The announcement has come as a shock to many people within the industry as it was originally introduced to help retirees cope with market volatility throughout the COVID-19 pandemic. Now the markets have recovered to near all-time highs.

Pension halving legislation

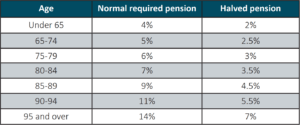

The original legislation states “the government has reduced the minimum annual payment required for account-based pensions and annuities, allocated pensions and annuities and market-linked pensions and annuities by 50% for the 2019–20, 2020–21, 2021–22 and 2022-23 financial years.” This minimum pension is calculated as at 1 July each financial year and is calculated as a percentage of the pension balance. This is the minimum pension that must be paid to beneficiaries for the fund to remain compliant.

An example of this would be a 65 year old retiree with a superannuation fund in drawdown/pension mode valued at $700,000. Under normal circumstances, the minimum pension drawdown would be $35,000 (5%). With the pension halving legislation in place, this same individual would only be required to draw $17,500 (2.5%).

Benefits

The major benefit to the pension halving continuation is it allows retirees to preserve their super balance which serves as a tax haven. All income from investments and capital gains that are made within this environment are tax free.

Not being required to crystallise losses in volatile market conditions. Although the markets have recovered from the COVID-19 sell off, there is still a lot of volatility in the markets today with inflationary concerns and continuing geopolitical issues in Europe.

Key takeaways

- Pension halving is not mandatory. Individuals will need to review their situation and assess if pension halving will be of benefit.

- This legislation will apply to account based, transition to retirement and term allocated pensions.

If you would like to take advantage of this legislation, please reach out to your Financial Adviser.

Please note this article provides general advice only and has not taken your personal, business or financial circumstances into consideration. If you would like more tailored advice, please contact us today.