Generally speaking, there are two ways to make more money in life: by working day in, day out, or by letting your money and assets work for you. Now I can only speak for myself, but letting my assets work for me sounds much better than grinding away at the office for the rest of my life (not that I don’t love my job!).

It may sound like prudent practice, but leaving your entire life savings under a mattress will not give you any return or increase in capital (in fact, after inflation your buying power has actually decreased). Even leaving your money in a bank account will only generate a minimal return. On the other hand, investors can earn additional money through dividends and distributions from their investments or by purchasing assets that increase in value.

The purpose of this article is to introduce you to the world of investing and provide clarity on key concepts that we are often asked about by our clients.

When should I start investing?

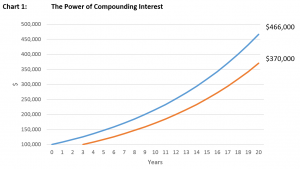

If we ignore transaction costs and the cyclicality (ups and downs) of markets, the answer to this question would be an easy one: RIGHT NOW! The power of compounding interest means that you are better off investing as soon as possible so your future returns are off a higher base. This concept is best conveyed in the chart below. Chart 1 shows that an individual who invests $100,000 today (Blue) for 20 years at an 8% return will earn $96,000 more than an individual that invests the same amount, earning the same return, only 3 years later (Orange). In the fourth year, Blue would earn 8% on $126,000 ($10,000) whereas Orange would earn 8% on the initial $100,000 ($8,000). Therefore, it seems the early bird gets the worm after all!

How much should I start investing with?

Unfortunately, for us investors, we do live in a world with transaction costs such as brokerage so it can be unwise to invest small amounts of money where your returns will be “eaten up” by these costs. A common brokerage fee structure for a number of retail stockbroking firms (including our own) is:

- $55.00 for trades up to $10,000

- 55% for trades over $10,000

As an example, if I buy $15,000 worth of shares and sell them a year later for $16,500, I would earn $1,500 in capital gains minus $173 in brokerage (buying and selling) to have a net capital gain of $1,327. This example shows that a reasonable capital return of 10% has been reduced to 8.8% after fees. Now, imagine if I only invested $1,000 and sold my shares for $1,100. My $100 (10%) capital return would reduce by $110, leaving me with a measly -1% return – which isn’t very sexy at all.

So, what does this all mean? If you are an individual that wishes to purchase some Australian shares, I would recommend building up cash to a level that minimises the ratio between brokerage/investment. If you are interested in creating a portfolio with a number of assets, I would recommend coming into one of our offices for a consultation (if you are good at something, you don’t do it for free).

How much risk should I take?

This is an extremely important question and one that can be the difference between living comfortably in retirement or couch surfing at your grandkid’s place. The amount of risk you take on is also dependent on your investment goals. For example, an 85 year old trying to provide for their retirement would have a much more conservative approach to investing than a 28 year old who is trying to build wealth to purchase their first home.

In addition to understanding your goals, at our firm, and in the advising community as a whole, we require our clients to complete a risk profile questionnaire, which provides a clearer picture of exactly how to risk averse they are. The results of this questionnaire then distinguishes which risk profile our clients fall into and how their money should be invested. The financial advisory industry uses five risk profiles:

- Conservative

- Moderately conservative

- Balanced

- Growth

- High growth

What should I invest in?

The answer to this question is a direct result of what risk profile you are aligned with. There are five main asset classes that we invest in at our firm. They are, in ascending order of riskiness:

- Cash

- Fixed interest: corporate, government or semi-government debt

- Property and infrastructure: shares or holdings in property and infrastructure assets

- Australian shares: shares listed on the ASX

- International shares: shares listed on foreign stock exchanges

The proportion of your wealth that you should invest in each asset class is dependent on your risk profile. For example, a balanced portfolio at our firm invests 5% in cash, 35% in fixed interest, 20% property, 30% Australian shares and 10% international shares. The holdings in cash and fixed interest will ensure that 40% of your portfolio is invested in assets that will preserve your capital while paying some income. The 20% of property holdings provides investors with the potential for capital gains while maintaining some level of capital preservation and income. The 40% held in Australian and international shares provides exposure to riskier assets that can provide greater capital gains and income in the form of dividends.

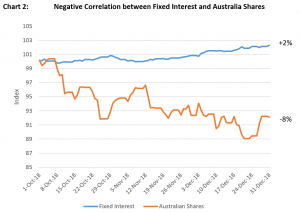

Another benefit of investing in different asset classes is to diversify your portfolio and take advantage of the low, or even negative, correlation between some investments. Correlation is a mutual relationship between two variables (assets). By way of example, Chart 2 shows how the defensive fixed interest asset class increased by 2% from October to December 2018 as investors fled the riskier Australian shares asset class that decreased by 8% over the same period. If you were invested entirely in Australian shares, you would have lost 8% of your capital whereas you have only lost 3% if you were invested 50/50 across the asset classes.

If you have been going to sleep on a mattress full of your life savings every night, or if you are interested in learning more about investing, please feel free to come into one of our offices to have a chat. Our investment team relishes any opportunity to educate people on the benefits and techniques of investing and there is nothing more satisfying than helping others unlock the power of sitting back, and letting your money work for you.

Please note, this article provides general advice and information only. It has not taken your personal or financial circumstances into consideration. If you would like more tailored investment or financial advice, please contact us today.