“I’ve just received a letter from XYZ Superannuation Fund saying I have an account with them. What does this mean and how did I get any money in the account?”

This is the annual benefits statement provided each year by all superannuation funds. It is a report to members of the fund that tells the member:

- How much their employer has paid into the fund during the last financial year

- How much was paid to the fund for the administration of your benefit

- What insurance is held through the fund

- How the investments performed during the year

- What investment option your benefits are invested in

- Your total balance

- Whether you have made a beneficiary nomination

“I can see all of that stuff but I don’t know what it means. Can I draw this money out for a holiday?”

No, superannuation is accumulated through compulsory contributions made by your employer during your working life, and you can’t draw from it until you reach at least 60 years of age.

“Wow that’s a long time, and a bit of a waste of time if you ask me.”

Yes, it is a long time but it is not a waste of effort. Your employer must pay 9.5% of your salary every year into the fund of your choice – imagine how much that might be in 40 years’ time! Let’s say that your salary is $55,000 per year now – that means your employer has to add at least $5,225 to your fund every year, and the contributed amount will increase every time you get a pay rise. Some of the amount contributed is paid out in tax, and the rest is invested with the object of growing over time. How much it grows will depend on the investment option or asset allocation that you choose.

The Fund must advise you how much you have paid to them in administrative fees during the year. This section is important. Take some time to compare the fees you have paid in your account with fees in other funds. If your fund is very expensive compared with others, then consider switching funds.

You must compare ‘apples with apples’ – don’t look at a High Growth fund and compare that with a Moderately Conservative fund. The rate of growth may be significantly different and the fees may also be different.

Has your fund performed as well as or better than the fund you compare it with? For example, if your Balanced fund has returned 7.8% in the last financial year and other Balanced funds you have checked are returning 10% for the year, it may be prudent to look a little closer at your own fund and potentially consider a switch.

Check performance over a longer timeframe – 1 year out-performance is good, but has your fund outperformed over 5 years or more? If not, you may want to look more closely and potentially find a fund that has a better longer-term performance.

Switching decisions should be based on long term performance coupled with the rate of fees you pay each year. Remember that switches come with a cost so you need to have good reason to do so.

“How did I get all of these super funds?”

When you begin a job, you should advise your employer where you want your contributions paid. If you don’t do this, then the employer will send your contributions to the fund it uses by default and that creates a new super account. If you have had a number of jobs and you now have more than one account, you should research all the funds to discover the better performing or lower cost fund, and consolidate (rollover) your benefits into the one account. Make sure you advise your employer if this account is not the one where they are currently paying your contributions.

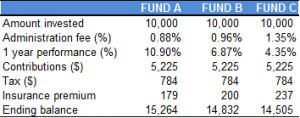

Here’s an example comparison between 3 funds, made on these assumptions:

- Salary $55,000

- Starting balance $10,000

- Life, TPD & Income Protection insurance in each fund

You can see a big difference in the ending balance between the 3 funds because of the rate of fees, the 1-year performance and the insurance premium paid. If you are invested in Fund C, should you be rolling over to Fund A? You must do the homework to ensure that the long-term performance of Fund A is consistently good. You want to have your benefit invested in a fund that can give you a good and consistent return over a longer period than 1 year.

“Why am I paying for insurance?”

Have a look at the insurance section on your statement so that you know what insurance coverage you have. You may have a default amount of life and/or total and permanent disablement (TPD) cover. Life insurance pays a benefit to your family in the event of your death, but TPD will pay a benefit that you can draw on if you are totally and permanently disabled. Be aware that the sum for which you are insured is likely to decrease as you age. This is important, as you may be grossly underinsured at a time where it is most needed.

The other type of insurance you may have is income protection – this one replaces part of your salary if you are unable to work through illness or injury. Check the premium on your insurances, and check waiting and benefit periods on the income protection policy.

If you consolidate funds, you will lose insurance benefits in any of the funds you roll out of so be aware you may then not have sufficient, or any, insurance. You should consult a qualified professional for insurance advice.

Nominating a beneficiary to receive your benefit upon your death, and keeping this nomination current, is important. Many nominations lapse in 3 years from when they were made, so you should regularly check your nomination remains current. Another thing to look out for is a nomination made to an ex-spouse. If you separate from your partner, you should make a new nomination. If you don’t, then your benefit is going to be paid to that ex-spouse, even if you have entered another marriage.

Please note this article provides general advice only and has not taken your personal or financial circumstances into consideration. If you would like more tailored financial or superannuation advice, please contact us today. One of our advisers would be delighted to speak with you.