And we’re not even halfway through it…

It’s certainly been an interesting few months, with the threat of potential changes to the financial planning landscape that would probably have occurred if the federal election result had gone the other way.

As the great Ronald Dale Barrassi once said, “The only constant in life is change.” It’s fair to say everyone in our industry; from clients to those earning a living in it, are looking forward to some stability for the time being.

With the election now a thing of the past and the end of the financial year upon us, it’s time to review some of the strategies that assist with our wealth accumulation objectives.

1. Give your super a free kick

Now is a good time of the year to make additional contributions into super, especially if you intend to claim those contributions as a tax deduction.

Any surplus cash you have sitting in a bank account earning the current abysmal rate of interest can be contributed into super before June 30 as a ‘personal’ contribution and claimed as a tax deduction.

Providing you haven’t exhausted your $25K concessional contribution cap, that increased tax deduction will most likely result in you obtaining an increased refund from the ATO.

The benefits are twofold; you get an increased tax refund which can be directed however you wish whilst also increasing the wealth you have accumulating in super.

2. Utilising unused concessional contributions

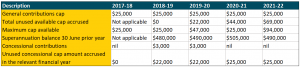

From 1 July 2018, if you have a total superannuation balance of less than $500K as at 30 June the previous financial year, you will be able to contribute more than the general $25K concessional contributions cap for that year by topping up the contribution with the ‘unused’ concessional cap from prior years.

Here’s how it will work:

In the table above, this individual in the 2019-20 year could potentially make a concessional contribution of up to $47K because they had used $3K in the prior year thereby having an ‘unused’ balance of $22K that can be carried forward into the next year.

In the 2020-21 year, because the balance of their super was above $500K on 30 June 2020, the concessional contributions cap is limited to the yearly amount of $25K. In the subsequent year, 2021-22, the ball game has really opened up due to the super balance dropping below $500K at 30 June 2021 which has provided an opportunity to contribute up to $94K in that year.

This potentially allows for realised capital gains to be ‘transferred’ into super and be taxed at the 15% contribution rate, as opposed to a higher marginal tax rate because the concessional contribution can be claimed as a tax deduction.

This is a strategy to keep in mind over the coming years especially if you’re approaching retirement and have a sizeable amount invested outside the super environment that has significant unrealised capital gains.

3. Check in on your goals

It’s a good time of the year to check in on your life and financial goals to see if you’re on target to making your dreams become a reality. Similarly, expectations may need to be revised to take account of changes to your circumstances over the last 12 months that have impacted on your wealth accumulation strategies.

At the end of the day, your super is your money and you are ultimately responsible for how it performs and grows. You need to ensure it is being invested wisely and in line with the timeframe you intend to access it.

Here’s hoping for more stability and certainty on the financial planning front over the next 12 months, at least!

Please note this article provides general advice only and has not taken your personal or financial circumstances into consideration. If you would like more tailored financial or superannuation advice, please contact us today. One of our advisers would be delighted to speak with you.