Government support comes in all shapes and sizes and the temporary minimum pension drawdown relief was one key measure designed to support retirees at the onset of COVID-19. Superannuation pensions and annuities are subject to rules that determine the minimum and maximum amounts to be paid in a financial year. The legislation allowed superannuation accounts that are currently in drawdown/pension mode to effectively halve their annual drawdown limits and preserve superannuation balances during the COVID-19 market sell-offs.

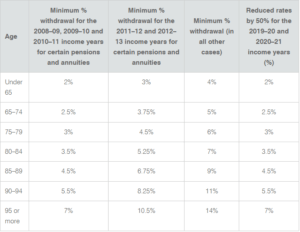

These rules were initially legislated for the 2019/20 and 2020/21 Financial Year’s (FY):

Referencing the above table, a retiree aged between 65-74 would normally need to draw a 5% minimum amount per annum from their pension accounts. The drawdown relief legislation allows this individual to draw only 2.5%. This preserves the superannuation balance and avoids the need to sell down investments during the height of the market sell-offs.

An example would be a retiree aged 65 with an $800,000 pension balance. Under normal circumstances, 5% must be drawn per annum, which is $40,000. However, with the drawdown relief in place, only 2.5% is required to meet the annual legislated drawdown requirements, which is $20,000.

Benefits of this temporary measure to retirees

- Preservation of superannuation balance (tax-free nest egg).

- Avoids crystallising losses (from the volatile COVID-19 sell-offs).

- Flexibility on where to draw income (access taxable sources before superannuation).

On Saturday 29 May 2021, the government announced that a further extension to this measure is being considered for the 2021/22 FY.

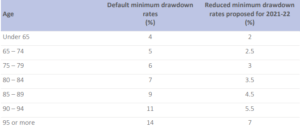

The proposed minimum pension drawdown for 2021/22 FY:

Key takeaways from the May announcement

- This proposal is not yet law and still needs to be tabled.

- This measure is not compulsory. Individuals need to review their situation to assess whether the pension halving/reduction will benefit their unique circumstances.

- The measure will apply to account-based, transition to retirement and term allocated superannuation pensions.

Please keep in mind that there are no guarantees that the temporary minimum pension drawdown relief will be extended into the 2021/22 FY. This is something that we are keeping a close eye on for the benefit of our clients.

If this is something you’d like to take advantage of, please reach out to your Financial Adviser.

Please note this article provides general advice only and has not taken your personal, business or financial circumstances into consideration. If you would like more tailored advice, please contact us today.