Given the escalating numbers of COVID-19 cases in Australia, we have had to change our lifestyle very quickly to incorporate social distancing and more recently put up with state-wide lockdowns. The government has made a series of announcements on the 22nd of March 2020 which are designed to provide support to people impacted by the virus.

The new measures announced are predominantly in the area of Superannuation legislation and social security.

Summary of these measures;

- Reduction in minimum pension

- Early access to super benefits

- Reduction in social security deeming rates for the incomes test

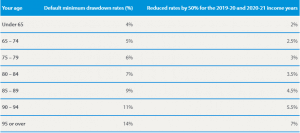

Reduction in minimum pension

Across the board, minimum pension drawdown rates for market linked income streams are reduced by 50% for the 2019/20 and 2020/21 financial years. The aim of this measure is to support retirees who are not required to draw the current pension minimums and can reduce pension drawdowns to avoid selling investments in a depressed market.

This will not affect you if you need the current minimums to survive, already drawing above the minimum pension or currently drawing an income from a complying lifestyle pension.

Early Access to super benefits

Access to superannuation benefits will be opened up from mid-April. The temporary access allows affected individuals to access up to $10,000 in each of the 2019/20 and 2020/21 financial years for a maximum of $20,000 of tax-free superannuation withdrawals.

You must meet the following criteria’s to qualify;

- You are unemployed

- You are eligible to receive a JobSeeker Payment, Youth Allowance for job seekers, Parenting Payment, Special Benefit or Farm Household Allowance

- On or after 1st of January 2020, you were made redundant or your working hours were reduced by 20% or more or if your businesses was suspended as a sole trader.

This is designed to be a last resort for those with no other means of attaining funds to meet their current living expenses.

However, this could be a huge trap for those who utilise the withdrawals by meeting the above conditions but do not actually require the funds. Younger Australians in the early stages of building their super could be most at risk, as they could take funds out of super just for the sake of security. Given the power of compound interest, removing $20,000 from a super fund 20 or 30 years prior to retirement access could have a devastating impact on their final retirement balance.

Reduced social security deeming rates

A direct loosening to Centrelink’s income test, whereby the upper and lower social security deeming rates will be reduced from 1st of July 2020 to 0.25% up to the threshold and 2.25% above the threshold. This is an overall reduction of 0.75% from the default 1% up to the threshold and 3% above the threshold.

An individual with $550,000 in financial assets on the default deeming rates of 1% and 3% will have their age pension reduced by $65 each per fortnight. Under the new transitional deeming rates, their pensions will only be reduced by $32 per fortnight. The key to consider is that deeming is only a part of the incomes derived by the client, which is dependent on the level of financial/investable assets and the loosening of the deeming rates will not help if your prevailing test is the Assets test.

Further measures are set to be announced in the coming weeks, however, it seems as though these initial changes will provide relief to those who are impacted.

Please note this article provides general advice only and has not taken your personal, business or financial circumstances into consideration. If you would like more tailored advice, please contact us today.