Clients often wonder why as advisers we explore client’s risk profiles, and what does it really do? Risk profiling is a process for determining appropriate investment asset allocations for each investor. There is no right or wrong answers, only what suits you.

The key components for establishing a risk profile are:

- What is the level of risk the client is comfortable taking?

- How much financial risk can a client afford to take?

- How much risk is required to achieve the goals with the financial assets at the client’s disposal?

What risk is a client willing to take?

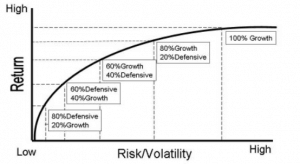

At some point you will have encountered the classic risk vs return curve, that is to get the most return you must take the most risk. The lure of the high prize must be traded off against the risk of significant loss. Like at a casino, the odds are not always in your favour and a high-risk strategy can see high volatility and sharp rises and falls in a client’s portfolio. This may appeal to some clients but to others, this is a nightmare, it could mean an extension of your working career rather than early retirement or vice versa. Generally speaking, age is often a key factor associated with risk tolerance, the younger we are the more risk we are willing to accept and as we age, we slide back along the risk curve to a less risky asset allocation. This is often termed as reducing “sequencing risk”.

How much financial risk can a client afford to take?

This component will often consider two items, stage of life and the number of assets available. The younger we are, we have greater time to recover and rebuild from a financial setback. Similarly, if we have a higher amount of financial assets at our disposal, we may choose to allocate a higher percentage of these targeting greater returns knowing we still have a sound financial base to fall back on.

How much risk do my goals need?

Something that many people ignore is that to achieve their goals, they simply do not need to take excessive levels of risk. The ability to recognize and discuss this is something to work through with your financial adviser. Similarly, sometimes goals require a level of risky investment that is inappropriate to a client. Discussion over conflicting goals and risk is very important to ensure you get the right investment plan for you.

Through each of these components of risk profiling, there are some common factors and gaining an understanding of these factors for each client is critical in the development of financial plans:

- Goals – what is it, how much, and what is the priority?

- Timeframe – what is the timeline for each of your goals?

- Investment capital – how much do you have to build wealth?

- Client age – how far into your life cycle are you?

- Liquidity, Income and Growth – do you require liquid funds for lump sum expenditure, do you require regular income from investments, are you focused on growth only?

In summary, the main issue isn’t if you have a high growth, balanced or conservative profile, the most important aspect is that your risk profile reflects you and your personal circumstances. Risk profiling is important for an adviser to review regularly with clients to ensure the clients’ thoughts and preferences have not changed over time and that the investment remains appropriate.

Please note this article provides general advice only and has not taken your personal, business or financial circumstances into consideration. If you would like more tailored advice, please contact us today.