Retirement is something that most people look forward to but not everyone plans and prepares for. Often it is not good enough to be emotionally ready to retire but it is crucial to ensure that you are financially ready too. Before you walk away from a career that you have been immersed in for years and run off into the sunset, it is important to consider your goals and objectives.

- Do you still enjoy work and how much longer can you go on for?

- Do your retirement goals fall in line with your partner?

- How is your physical and mental health?

- Do you have a healthy financial situation (dependants and debts)?

If you can tick all these boxes then you should be ready to plan for retirement. Key areas to consider include;

- How much money will you need? If you run a household budget, consider how that is likely to change when you retire.

- What lifestyle aspirations do you have for retirement? You may wish to partake in international holidays once each year or caravan around Australia. Factoring in your lifestyle goals will help answer the question of whether you have enough.

- What legacy aspirations do you have? Some may be comfortable for the kids to receive whatever is left, others may have a preference of leaving something behind as part of their legacy or even providing assistance in the near future.

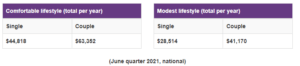

The Australian Financial Security Authority (AFSA) has deemed the following incomes as adequate for a ‘comfortable’ or a ‘modest’ lifestyle in retirement.

As part of your retirement plan, it is also important to be mindful of common risks as you approach or enter retirement.

- Sequencing risk – this is the risk of the market facing a severe and unexpected downturn just before you retire. As a pre-retiree, you may not have the time horizon to wait out a recovery. An example would be a retirement nest egg of $1,000,000 falling to $750,000 just as you are about to retire. At a drawdown of 5%, this is a reduction of annual income from $50,000 pa to $37,500 pa and a big hit to anyone’s retirement.

- Lower than expected returns – retirement portfolios are not designed to shoot the lights out but to generate a sustainable level of return with a focus on capital preservation. However, if returns do not stack up for whatever reason, it will lead to a rapid deterioration of your capital and your retirement savings may not last as long as you designed them to.

- Longevity risk – this is the risk of retirees living beyond their retirement savings. With improved health care and higher standards of living, life expectancy is higher than ever. Hence, with all else equal, you are more likely to outlive your retirement savings.

If you wish to seek assistance on your retirement plan, please reach out to one of our friendly financial advisers.

Please note this article provides general advice only and has not taken your personal, business or financial circumstances into consideration. If you would like more tailored advice, please contact us today.